AI exuberance: Economic upside, stock market downside

.

Financial markets are exuberant—and there are some good reasons for that. Despite megatrend headwinds in 2025 like demographic slowdowns and rising tariffs, economies held firm. U.S. corporate earnings growth and fundamentals stayed strong, powered by AI investment and other positive technology shocks.

Our data-driven megatrends framework shows these supply-side forces will shift again in 2026. How well AI investment will counteract negative shocks shapes our economic outlook. Over the next five years, we see an 80% chance that economic growth diverges from consensus expectations. These projections shape our investment outlook and offer somewhat unconventional —yet increasingly compelling—investment opportunities for increasingly frothy financial markets.

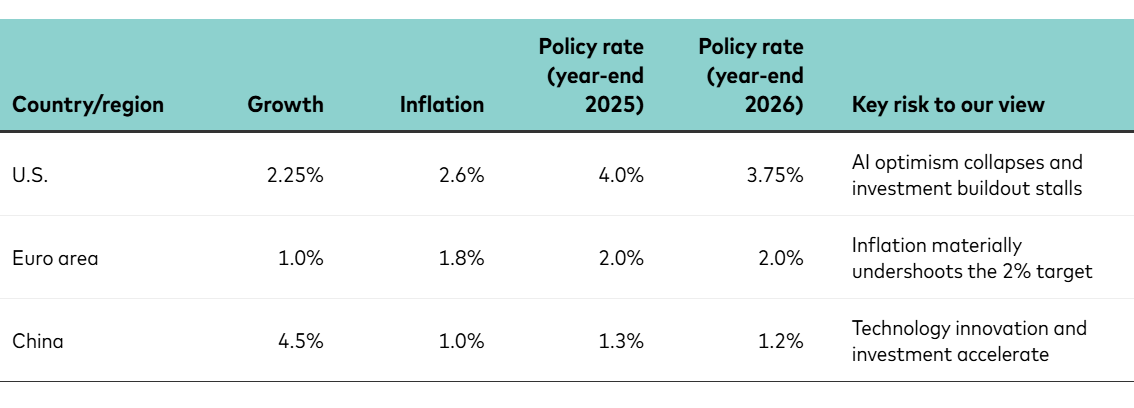

Vanguard’s 2026 economic forecasts

Notes: Forecasts are as of November 20, 2025. For the U.S., growth is defined as the year-over-year change in fourth-quarter GDP. For the euro area and China, growth is defined as the annual change in GDP in the forecast year compared with the previous year. Inflation is core inflation and thus excludes volatile food and energy prices. For the U.S. and the euro area, core inflation is defined as the year-over-year change in the fourth quarter compared with the previous year. For China, core inflation is defined as the average annual change compared with the previous year. For the U.S., core inflation is based on the core Personal Consumption Expenditures Index. For the euro area and China, core inflation is based on the core Consumer Price Index. For U.S. monetary policy, Vanguard’s forecast refers to the top end of the Federal Open Market Committee’s target range. The euro area’s policy rate is the deposit facility. China’s policy rate is the seven-day reverse repo rate.

Source: Vanguard.

Higher growth is on the horizon, particularly for the U.S.

We anticipate that AI will stand out among other megatrends, given its capacity to transform the labour market and drive productivity. AI investment’s outsized contribution to economic growth represents the key risk factor in 2026.

The ongoing wave of AI-driven physical investment is expected to be a powerful force, reminiscent of past periods of major capital expansion such as the development of railroads in the mid-19th century and the late-1990s information and telecommunications surge. Our analysis suggests that this investment cycle is still underway, supporting our projection of up to a 60% chance that the U.S. economy will achieve 3% real GDP growth in the coming years—a rate materially above most professional and central bank forecasts.

But this future is not quite now. In 2026, the U.S. is positioned for a more modest acceleration in growth to about 2.25%, supported by AI investment and fiscal thrust from the One Big Beautiful Bill Act. The first half of the year may be softer given the lingering effects of the stagflationary megatrend shocks of tariffs and demographics, as well as yet-to-materialise broad-based gains in worker productivity. The labour markets, which cooled markedly in 2025, should stabilise by the end of 2026, helping the unemployment rate to stay below 4.5%.

Economic growth is expected to keep U.S. inflation somewhat persistent, remaining above 2% by the close of 2026. This combination of solid growth and still-sticky inflation suggests that the Federal Reserve will have limited scope to cut rates below our estimated neutral rate of 3.5%. Our Fed forecast is a bit more hawkish than the bond market’s expectations.

Given similar AI-related dynamics, our forecast for China’s economic growth is also above consensus expectations in 2026. Despite ongoing external and structural challenges, real GDP growth is more likely to register 5% than 4%.

Conversely, our risk assessment for the euro area is more consensus-like given the lack of strong AI dynamics. We anticipate growth to hover near 1% in 2026, as the drag from higher U.S. tariffs is offset by increased defense and infrastructure spending. Inflation should stay close to the 2% target, allowing the European Central Bank to maintain its current policy stance throughout the year.

A differentiated investment playbook

Our capital markets outlook differs across markets, asset classes, and investment time horizons. Overall, our medium-run outlook for multi-asset portfolios remains constructive, with positive after-inflation returns likely to continue. In 2026, U.S. technology stocks could well maintain their momentum given the rate of investment and anticipated earnings growth.

But let us be clear: Risks are growing amid this exuberance, even if it appears “rational” by some metrics. More compelling investment opportunities are emerging elsewhere, even for those investors most bullish on AI’s prospects. Our conviction in this view is growing, and it parallels investment returns in previous technology cycles.

Our capital markets projections show that the strongest risk-return profiles across public investments over the coming five to 10 years are, in order:

- High-quality U.S. fixed income.

- U.S. value-oriented equities.

- Non-U.S. developed markets equities.

We maintain our secular view that high-quality bonds offer compelling real returns given higher neutral rates. Returns should average near current portfolio income levels, representing a comfortable margin over the rate of expected future inflation. That’s the primary reason why bonds are back, regardless of what central banks do in 2026. Importantly, U.S. fixed income should also provide diversification in a world where AI disappoints, leading to lower growth—a scenario with odds that we calculate to be 25%–30%.

We remain most guarded in our assessment of U.S. growth stocks, which admittedly have outperformed most other investments by an astounding margin. Yet, as we will show in this outlook, our muted expected returns for the technology sector are entirely consistent with our more bullish prospects for an AI-led U.S. economic boom.

The heady expectations for U.S. technology stocks are unlikely to be met for at least two reasons. The first is the already-high earnings expectations, and the second is the typical underestimation of creative destruction from new entrants into the sector, which erodes aggregate profitability. Volatility in this sector—and hence the U.S. stock market overall— is very likely to increase. Indeed, our muted U.S. stock forecast of 4%–5% average returns over the next five to 10 years is nearly singlehandedly driven by our risk-return assessment of large-cap technology companies.

The history of investing during technology cycles reveals some counterintuitive—yet increasingly compelling—investment opportunities regardless of whether AI proves transformative or not. Both U.S. value-oriented and non-U.S. developed markets equities should benefit most over time as AI’s eventual boost to growth broadens to consumers of AI technology. Economic transformations are often accompanied by such equity market shifts over the full technology cycle.

Overall, these three investment opportunities are both offensive and defensive. This risk assessment holds, no matter whether today’s AI exuberance ultimately proves rational or not.

Notes:

All investing is subject to risk, including the possible loss of the money you invest. Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss.

Investments in bonds are subject to interest rate, credit, and inflation risk.

Investments in stocks and bonds issued by non-U.S. companies are subject to risks including country/regional risk and currency risk. These risks are especially high in emerging markets.

IMPORTANT: The projections and other information generated by the Vanguard Capital Markets Model (VCMM) regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. VCMM results will vary with each use and over time.

The VCMM projections are based on a statistical analysis of historical data. Future returns may behave differently from the historical patterns captured in the VCMM. More importantly, the VCMM may be underestimating extreme negative scenarios unobserved in the historical period on which the model estimation is based.

The Vanguard Capital Markets Model® is a proprietary financial simulation tool developed and maintained by Vanguard's primary investment research and advice teams. The model forecasts distributions of future returns for a wide array of broad asset classes. Those asset classes include U.S. and international equity markets, several maturities of the U.S. Treasury and corporate fixed income markets, international fixed income markets, U.S. money markets, U.S. municipal bonds, commodities, and certain alternative investment strategies. The theoretical and empirical foundation for the Vanguard Capital Markets Model is that the returns of various asset classes reflect the compensation investors require for bearing different types of systematic risk (beta). At the core of the model are estimates of the dynamic statistical relationship between risk factors and asset returns, obtained from statistical analysis based on available monthly financial and economic data from as early as 1960. Using a system of estimated equations, the model then applies a Monte Carlo simulation method to project the estimated interrelationships among risk factors and asset classes as well as uncertainty and randomness over time. The model generates a large set of simulated outcomes for each asset class over time. Forecasts represent the distribution of geometric returns over different time horizons. Results produced by the tool will vary with each use and over time.

This article contains certain 'forward looking' statements. Forward looking statements, opinions and estimates provided in this article are based on assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are based on interpretations of current market conditions. Forward-looking statements including projections, indications or guidance on future earnings or financial position and estimates are provided as a general guide only and should not be relied upon as an indication or guarantee of future performance. There can be no assurance that actual outcomes will not differ materially from these statements. To the full extent permitted by law, Vanguard Investments Australia Ltd (ABN 72 072 881 086 AFSL 227263) and its directors, officers, employees, advisers, agents and intermediaries disclaim any obligation or undertaking to release any updates or revisions to the information to reflect any change in expectations or assumptions.

GENERAL ADVICE WARNING

Vanguard Investments Australia Ltd (ABN 72 072 881 086 / AFS Licence 227263) (VIA) is the product issuer and operator of Vanguard Personal Investor. Vanguard Super Pty Ltd (ABN 73 643 614 386 / AFS Licence 526270) (the Trustee) is the trustee and product issuer of Vanguard Super (ABN 27 923 449 966). The Trustee has contracted with VIA to provide some services for Vanguard Super. Any general advice is provided by VIA. The Trustee and VIA are both wholly owned subsidiaries of The Vanguard Group, Inc (collectively, “Vanguard”).

We have not taken your or your clients' objectives, financial situation or needs into account when preparing our website content so it may not be applicable to the particular situation you are considering. You should consider your objectives, financial situation or needs, and the disclosure documents for the product before making any investment decision. Before you make any financial decision regarding the product, you should seek professional advice from a suitably qualified adviser. A copy of the Target Market Determinations (TMD) for Vanguard's financial products can be obtained on our website free of charge, which includes a description of who the financial product is appropriate for. You should refer to the TMD of the product before making any investment decisions. You can access our Investor Directed Portfolio Service (IDPS) Guide, Product Disclosure Statements (PDS), Prospectus and TMD at vanguard.com.au and Vanguard Super SaveSmart and TMD at vanguard.com.au/super or by calling 1300 655 101. Past performance information is given for illustrative purposes only and should not be relied upon as, and is not, an indication of future performance. This website was prepared in good faith and we accept no liability for any errors or omissions.

Important Legal Notice - Offer not to persons outside Australia.

The PDS, IDPS Guide or Prospectus does not constitute an offer or invitation in any jurisdiction other than in Australia. Applications from outside Australia will not be accepted. For the avoidance of doubt, these products are not intended to be sold to US Persons as defined under Regulation S of the US federal securities laws.

© 2025 Vanguard Investments Australia Ltd. All rights reserved.

Joe Davis, Global Chief Economist

26 November

vanguard.com.au