What to look for when choosing a financial adviser

.

We believe financial advice is essential for Australians looking to build wealth and reach their goals, whether in the early stages of their career or during retirement.

Financial advice adds tangible improvement to client outcomes, through suitable asset allocation, cost-effective implementation, and spending strategies. Not to mention the emotional value of advice, which is often underappreciated.

Everyone has different advice needs—from the simple to complex. But there are some fundamental elements that everyone should look for when assessing their adviser. Here are five of the most critical factors to help you make the right choice.

1. They take the time to understand you

Personal finances can be an intimate topic. Which is why the best advisers take the time to get to know you—whether it’s your interests, aspirations or motivations—before jumping into your financial situation.

Understanding helps to build trust and make you feel more comfortable having money-related conversations. But it’s also critical for identifying and setting appropriate financial goals.

In addition to investment advice, the role of your adviser is to help you navigate spending decisions, superannuation, cashflow management, insurance, estate planning, and a host of other issues. None of this is possible without an understanding of what you value, your attitude to risk, and what you’re striving towards.

Everyone is different, which is why tailored advice centred on your personal goals is necessary to give you the best chance of achieving the life you want.

2. They have a clear investment philosophy

You can think of your adviser’s investment philosophy as a roadmap for how they manage your money. It’s an encapsulation of how they believe markets work and how they can help you reach your investment goals.

For example, do they believe markets are largely efficient or prone to bouts of irrational exuberance? How do they match your investment strategy with your risk appetite? How do they manage the costs of investing while keeping your portfolio on track to meet your goals?

You don’t need to understand the ins and outs of markets and portfolios, but you should be able to understand your adviser’s philosophy.

A good investment philosophy will encourage you to take a disciplined, long-term view of your wealth. It should be distilled into a set of core investment principles that guide your adviser’s investment recommendations, set expectations, and help you manage setbacks.

3. They coach you through the market’s ups and downs

Investing is inherently emotional. When markets are tracking higher, you may be content to follow our long-term investment plan. But when market volatility sets in, you may begin to question your approach.

As the role of advice evolves, advisers are becoming more than just practitioners. They’re becoming financial coaches for their clients, guiding them to decisions that align with their long-term goals and interests.

Going it alone is difficult. A good adviser can help you develop a plan that’s tailored to your individual needs. Once a plan is in place, they can help you navigate the emotional side of markets by providing perspective, expertise, and insight into investor behaviour.

A good adviser will also listen to their clients’ concerns and help them make any sensible changes to their portfolio while reinforcing their long-term plan. They educate their clients along the way, instilling trust and confidence, and offer praise when their clients exercise discipline and follow through on their plan.

4. They use technology to enhance the human elements of advice

Technology is no substitute for real human connection. But the right technology used effectively can enhance your advice experience and make some processes simpler—while leaving more room for the human touch.

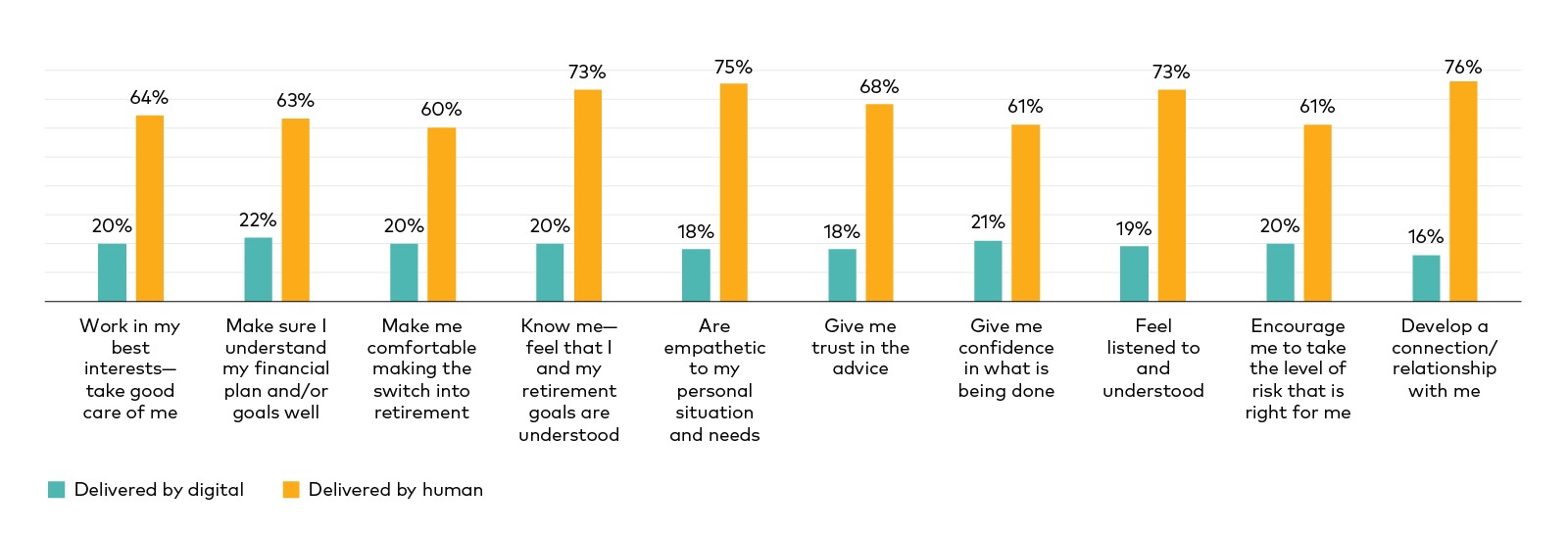

A Vanguard survey of more than 1,500 advised investors found that most prefer dealing with human advisers when it comes to advice delivery. In fact, 76 per cent said that if they decided to leave their current adviser they would switch to another person (not a digital service).

Figure 1. Investors prefer emotional and financial-planning services to be delivered by humans

Notes: In this figure, all 1,518 clients answered the question. They were presented with the micro-interactions and asked to rate whether they preferred that service to be delivered by a human or a digital adviser. The ratings were presented on an 11-point scale, where 0 meant “Completely delivered by a human” and 10 meant “Completely delivered by a digital service.” Clients were considered to prefer human delivery if their rating was between 0 and 4 and digital delivery of the service if their rating was between 6 and 10.

Sources: Vanguard and Escalent, 2021.

However, technology does lend itself well to certain aspects of the advice process. For example, when it came to managing taxes and capital gains, accessing the most appropriate funds, diversifying investments, and accounting for different scenarios, respondents had a higher preference for digital solutions.

Technology can also make advice more rigorous and engaging. Advisers should have an intuitive understanding of when digital solutions are appropriate and when their clients want a human at the helm.

5. They’re focused on investment outcomes

Cost remains one of the most important factors that determine investment outcomes, and seemingly small differences in cost can add up to a lot over your investing life.

Managing investments costs—whether fees or trading costs—allows you to put more of your money to work.

Which is one of the reasons why index and diversified funds and ETFs are increasingly used as portfolio building blocks. They allow you to create a tailored, risk-adjusted portfolio that meets your investment needs while keeping investment costs low.

Low fees are now a permanent fixture of the indexing landscape. However, as important as it is to minimise fees, it should not be the overriding consideration. Ultimately, you need a high-quality investment solution that matches your goals and risk profile.

Index management may be a systematised process, but index managers can still provide an edge to investors through scale, experience, and expert daily management of portfolios.

Talk to your financial adviser

Fears about the future and what markets may bring are natural. A good adviser will have the right expertise but should also understand the emotional side of investing.

Advisers can help with a range of advice needs. But ultimately the value they provide lies in ensuring you can look to the future with confidence.

If you think you could benefit from advice, why not start the conversation with an adviser? Perhaps there’s someone you know who can recommend one.

Vanguard

18 February 2026

vanguard.com.au